Call 888-758-7346

2022 mortgage industry predictions

2022 mortgage industry predictions

Dec 17, 2021

The second calendar year of the COVID-19-era found those in the mortgage industry making hay while making way for shrinking margins as the number of new rate-and-term refinances started to decline from record highs.

While Arizent survey respondents offered their 2022 forecast earlier in the month, we also invited industry figures to have their say. Apart from the buzz around more mergers and acquisitions ahead, leaders from all sides of the business offer their best predictions for the market conditions that we can expect in the next 12 months.

https://www.nationalmortgagenews.com/list/2022-mortgage-industry-predictions

Rethinking lead generation for a post-pandemic world

Nov 24, 2021

As margins tighten, text messaging has taken on new importance in mortgage customer prospecting, with some lenders even using it as a method for distributing videos that aim to educate and entice consumers.

But whether more traditional contact methods, such as direct mail, are effective in the post-pandemic environment remains a question heavily debated among lenders as they face the prospect of having to put more effort and dollars into lead generation in 2022.

https://www.nationalmortgagenews.com/list/lead-generation-in-a-post-pandemic-world

Refinancing after forbearance? Make sure you know the rules

Refinancing after forbearance? Make sure you know the rules

June 28, 2021

Millions of American homeowners took advantage of generous breaks that allowed borrowers to skip mortgage payments with no penalty.

But if you’ve been in forbearance and now want to refinance, be sure to follow a few straightforward rules, says Richard Pisnoy, principal at Silver Fin Capital Group. To qualify for a refi after forbearance, you must have made three consecutive payments on your loan, and you have to formally ask your mortgage servicer for a release from forbearance.

Pisnoy spoke with Bankrate about what he’s seeing in the mortgage market.

https://www.bankrate.com/mortgages/forbearance-can-complicate-refi/

Home Equity Is Soaring — if You're Tempted to Borrow Against Your Home, Read This First

Home Equity Is Soaring — if You're Tempted to Borrow Against Your Home, Read This First

October 1, 2020

Home equity is the share of your home that you actually own — the difference between its market value and the money you owe on your mortgage. As Andrew Weinberg, principal and mortgage loan originator at SilverFin Capital, explains, “It’s the amount you would net if you sold your home and paid off your mortgage.

https://money.com/home-equity-rising-coronavirus-pandemic/

Mortgage Rate Forecast For Q4 2020

September 29, 2020

The $64,000 question as it relates to the financial markets and to the mortgage market is who will be our next president,” says Andrew Weinberg, principal at Silver Fin Capital Group. “At a minimum, it is fair to say that each candidate will have a different approach to the economy, taxes and how to best achieve growth.

https://www.bankrate.com/mortgages/mortgage-rate-forecast/

Richard Pisnoy quoted in a Bankrate article entitled, "Coronavirus is changing home appraisals — and some borrowers don’t need them at all."

May 4, 2020

Richard Pisnoy, co-founder and principal at Silver Fin Capital, a mortgage broker in Great Neck, New York, says he has seen a marked increase in mortgage waivers since the coronavirus began spreading. In the past, perhaps only 10 percent of borrowers qualified for appraisal waivers. Pisnoy estimates about a third of borrowers today are allowed to skip the pre-closing valuation. “The waivers are really a nice thing and save money for home buyers,” Pisnoy concluded.

www.bankrate.com/mortgages/coronavirus-is-changing-home-appraisals/

Richard Pisnoy quoted in MoneyWise about how to get super-low mortgage rates

Richard Pisnoy quoted in MoneyWise about how to get super-low mortgage rates

April 4, 2020

Rich Pisnoy, a partner in Silver Fin Capital, was quoted throughout an article which appeared in MoneyWise April 4, 2020 entitled "How to Score One of Those Super-Low Mortgage Rates for Your Refinance." Pisnoy speaks to consumers who have been laid off or furloughed, the importance of being able to act fast to lock in a rate, and if paying points make sense. Pisnoy notes: "Points are not a bad thing. Paying points helps consumers 'buy down' their mortgage rate — which also will lower their monthly mortgage payment.”

https://moneywise.com/a/best-tips-for-scoring-a-stellar-mortgage-refinance

With no loan limits and easy requirements, VA loans are more popular than ever

With no loan limits and easy requirements, VA loans are more popular than ever

Jan 20, 2020

Andrew Weinberg is principal of Silver Fin Capital Group. He says a VA mortgage is very popular today because we simply have more veterans and eligible borrowers these days.

“Plus, it provides below-market rates on a 30-year fixed-rate mortgage, with 100 percent financing,” says Weinberg. VA loan rates lately are about 0.30% lower than conventional rates, on average.

https://themortgagereports.com/59869/va-loans-becoming-more-popular-with-no-loan-limits

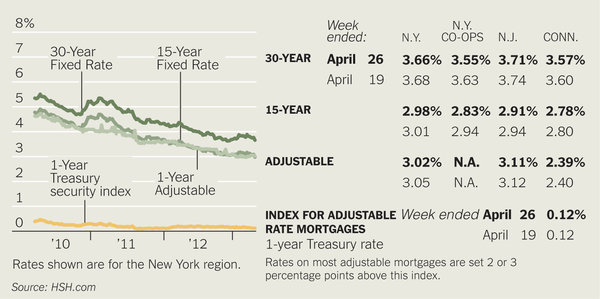

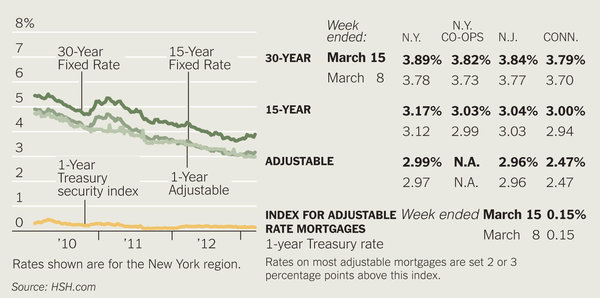

Mortgage Rates Hold On at Lowest January Levels Since 2013

Jan 17, 2020

"Homebuying and borrowing usually take a breather around the holidays and into the new year, but not this time," says Richard Pisnoy, a principal with Silver Fin Capital Group, a residential and commercial mortgage broker in Great Neck, New York, is quoted saying "The housing market is humming right now, and low mortgage rates are a big reason.”

https://moneywise.com/a/mortgage-rates-01-16-2020

'Can I Refinance While Buying a Second Home?' Here Are the Mortgage Rules

'Can I Refinance While Buying a Second Home?' Here Are the Mortgage Rules

April 2, 2019

As a buyer and a seller, you may be asking, "Can I refinance while buying a second home?" Maybe you've found a property that will be a killer investment at a bargain price. Or perhaps the beach cottage you've had your eye on for years just came on the market.

Whatever the reason, if you're considering applying for another loan while refinancing your current home, the process can be a bit complicated. To give you the full picture, we consulted mortgage experts and broke down the rules.

'Can I refinance an existing mortgage while buying a second home?'

There's nothing wrong with refinancing one mortgage at the same time that you are buying an investment property or second home with a mortgage, according to Andrew Weinberg, principal and licensed mortgage broker at Silver Fin Capital Group, in Great Neck, NY.

The key factor to making both the refinance and new purchase work is to ensure you will qualify for the new home loan.

"This means taking into account your current home payment," says Ralph DiBugnara, president of New York's Home Qualified and vice president at Cardinal Financial. A mortgage bank can very easily tell you the total payments and loan amounts you'll be able to carry based on your current income.

In some cases, you may even have to refinance to reduce your current mortgage payment to qualify for the new loan. Or you may need to cash out funds from the refinance to come up with the down payment on the new property.

The only ironclad rule is that you can't refinance a primary residence while applying for a mortgage on a new primary residence.

Consider working with one lender for both mortgages

The benefit of doing both loans—refinancing and obtaining a new mortgage—is that you can deal with a single loan officer and provide most of your documents (e.g., tax returns, W-2s, pay stubs, bank statements, etc.) only once.

You can also optimize your loan balances and your monthly payment to a degree by doing both loans with the same lender, says DiBugnara.

If you need to work with two different lenders, both need to be aware of the other loan.

When refinancing and buying at the same time isn't a good idea

You shouldn't refinance a home you intend to sell in the next six months or so because it's not cost-efficient.

"The closing costs don’t vary because you intend to pay off your loan in a short period of time," says Weinberg.

Additionally, most refinances have a clause stating the borrower must stay in the home for at least one year. This means you cannot refinance a primary residence, close on a second home, and then immediately move into it permanently.

The differences between an investment and second home

When applying for your second mortgage, your lender will take into account how you plan on using the property. So it makes a difference if the second home is for investment purposes or is a vacation home for personal use.

"If the home is an investment, you can use proposed rental income as an add-on to your second income when qualifying for the second mortgage," says DiBugnara.

But if you're purchasing a vacation home, the new debt will count 100% against your current income and could prevent you from qualifying for a refinance and a second mortgage.

The good news for those looking to buy a beach cottage or winter retreat? Vacation home mortgage rates are typically lower than investment home rates.

"You can also typically put less money down—sometimes just 10%," says Kylie Pak, owner of RedBrick Properties, in Richmond, VA, who specializes in property investing.

Too many people think it's OK to tap home equity to pay monthly bills

Too many people think it's OK to tap home equity to pay monthly bills

September 29, 2018

One in six homeowners in a new survey believed that it's OK to tap home equity to pay monthly bills — an attitude that sets financial planners' hair on fire.

Such thinking was most prevalent in the poll of 1,000 people among the lowest earners, less educated respondents and millennials.

Face reality

“If you are using your equity to pay your first mortgage or your utility bills, then that house is probably too expensive for you. That approach can’t last forever,” warns Andrew Weinberg, a principal with lender Silver Fin Capital Group in Great Neck.

Remember, if you can’t pay the money back, you can lose your home.

Turn to other alternatives

“Start doing a budget and sticking to it, and prioritize getting out of debt instead of going further into debt,” says Miller.

Build an emergency fund of at least 3 to 6 months of living expenses, so you have a cushion.

Consider your home sacred.

“When you’re nearing retirement and you need your equity the most, you’ll be tapped out," says Jared Weitz, founder of United Capital Source, a small business lender in Great Neck.

"There are many more sources for credit and personal loans today. Companies like Upstart, SoFi, LendUp and LendingClub can help bridge the gap during an emergency. Your home equity should be saved for retirement and looked at as a nest egg.”

Home Equity Loan Products –

Home Equity Loan Products –

HELOCs and HELs

JUNE, 2018

Andrew Weinberg, a partner at licensed mortgage originator firm Silver Fin Capital, explains more about these two products:

“HELOC and HELs are second mortgages. They’re riskier for the lender to take on, so the lender would expect to receive a premium for that risk in the form of higher interest rates and adjustable rates. For HELOCs, the interest rate is always adjustable; it is never fixed. The rate for a HELOC is typically based off the prime rate plus the lender’s ‘margin’ on top of that.”

“You might see a HELOC advertised as prime + 1% or even prime -0.25%. As the prime rate changes (either up or down), the interest rate on the HELOC will fluctuate. You can pay down the HELOC without penalty, and not pay interest on that outstanding amount anymore. And then you have access to those funds when you want or need them, which gives you more flexibility than with a HEL.

“HELoans are closed-end second mortgages,” explains Weinberg. “They usually have a fixed interest rate for some period of time. ‘Closed-end’ means that the loan amount is an agreed-upon amount before closing; each month, you pay interest and some principal.”

You could take out a 15 year home equity loan (or arrange for an even longer term). It might be based a 30-year amortization but the loan could be due in 15 years -- meaning you have to pay off or refinance the mortgage in 15 years, even though your payments were based on a 30-year loan. As a second mortgage, HELs have much higher rates than a typical first mortgage (probably 2-3% more than a first mortgage).

Weinberg adds,

“Second mortgages are usually smaller than the first mortgage. For example, a borrower might have bought a house for $800,000 with a $600,000, 30-year fixed-rate mortgage. A couple of years later, the homeowner decides they want to redo the kitchen and finish the basement. Let’s say the house is now worth $840,000, and the homeowner gets a $75,000 HELOC or HELoan to access the funds to do the work. They are cashing out some of their equity without touching the first mortgage.

“This might be a good option for the borrower who intends to pay the HELOC off in the near future. If you have a good deal on your first mortgage, you may not want to give that up by cashing-out the equity on your home. You can calculate your “blended” interest rate on both loans, and see how that compares to simply refinancing that first mortgage.”

Silver Fin's Richard Pisnoy selected as one of MPA Magazine's Hot 100

Silver Fin's Richard Pisnoy selected as one of MPA Magazine's Hot 100

FEB, 2018

MORTGAGE PROFESSIONAL AMERICA — In addition to being a productive loan originator in his own right, Richard Pisnoy has been instrumental in Silver Fin Capital’s continued success by creatively growing its large network of lenders and referral and lead sources, including developers, management companies and financial advisors. Pisnoy has been quoted as a mortgage expert in several print and online publications, including the New York Times and the Wall Street Journal.

“We all know that the mortgage business is a difficult industry, and Richard exemplifies the hard work, superior client service and vast expertise needed to be successful in this industry today,” a colleague says.

In addition to his work at Silver Fin Capital, Pisnoy remains active in his community through the Chad Strong Foundation and the Heroes to Heroes Foundation, a nonprofit organization that provides a spiritual healing, suicide prevention and peer support for veterans suffering from injury and PTSD. He was also appointed in 2017 to serve as a member of the Nassau County Police Department Foundation, which provides financial support to the analytic, operational and outreach components of the Nassau County Police Department.

What Airbnb Means for Your Mortgage

What Airbnb Means for Your Mortgage

DEC 20, 2017

In an article in U.S. News & World Report (12/20/17) entitled What Airbnb Means for Your Mortgage, Andrew Weinberg, principal and founder of Silver Fin Capital, is quoted explaining how operating as a B&B and using a spare room in your house blurs the line between primary residence and investment property. That could mean a less favorable interest rate following the refinancing because mortgages for investment properties are generally priced higher than mortgages on primary residences.

Stacey Elshehaby recognized as an “Elite Woman” in Mortgage

Stacey Elshehaby recognized as an “Elite Woman” in Mortgage

AUG 7, 2017

MORTGAGE PROFESSIONAL AMERICA — Mortgage Professional America has recognized Stacey Elshehaby as an Elite Woman in Mortgage. The award recognizes women in the mortgage business who are expertly leading and positively influencing the industry.

With more than 20 years of industry experience, there’s not much in the mortgage business that Stacey Elshehaby hasn’t seen. She joined Silver Fin Capital Group in 2008, and is now as Processing Department Manager is responsible for managing the company’s processing team and its loan pipeline for more than 50 wholesale lenders.

Also, a licensed loan originator, her deep and wide industry experience make Elshehaby invaluable to Silver Fin, says co-founder Andrew Weinberg. “This experience, coupled with a commitment to client service and loan officer support, makes Stacey one of the best loan processors in the business,” Weinberg says. “She is instrumental in helping the Silver Fin Capital team to offer the high level of professionalism and client service for which it has become known.”

Andrew Weinberg Chosen for

MPA’s Top 100

AUG 7, 2017

MORTGAGE PROFESSIONAL AMERICA — Andrew Weinberg was one of 100 individuals who was recognized by Mortgage Professional America for their achievements in 2016, and accomplishments that are expected in 2017.

Andrew, an experienced mortgage professional, co-founded Silver Fin Capital in 2005. He is responsible for all legal, financial, and administrative aspects of the business, including licensing and lender relations. Andrew is also responsible for the creation of Silver Fin Capital’s business development and marketing programs. His expertise spans all residential loans types, including conventional, FHA, jumbo/super jumbo, and co-op loans. Andrew is especially proud of how Silver Fin Capital has grown over the years by honing its processes and maintaining many long-tenured employees.

Prior to Silver Fin Capital, Andrew was an attorney in private practice, advising clients on various corporate, securities, and real estate matters. He also was senior vice president and general counsel of eBrainExchange, a developer of software applications for the corporate market. He spent several years in executive-level finance and legal roles at Nomura Securities, including Director of Legal Affairs for Operations and Information Technology, and Vice President and General Counsel of Nomura International Trust Company.

Andrew earned his Juris Doctor and MBA degrees from George Washington University, and a Bachelor of Science in Business Administration from the State University of New York at Albany. Andrew previously served as Trustee for the Village of Old Westbury, and is currently the Chairman of the Village's Architectural Review and Planning Board. His interests include classic cars, watching movies, and spending time with family.

Richard Pisnoy Chosen for MPA's Hot 100

Richard Pisnoy Chosen for MPA's Hot 100

DEC 4, 2014

MORTGAGE PROFESSIONAL AMERICA — A leader at a Great Neck, New York-based company has just received one of the mortgage industry’s highest honors. Richard Pisnoy, principal of Silver Fin Capital Group, has been named as one of Mortgage Professional America Magazine’s Hot 100 for 2014. This list, compiled annually, honors 100 people who have made waves in the mortgage industry over the last year. Honorees are nominated by their peers, and range from small-town mortgage brokers to CEOs of international companies. “The Hot 100 represents the best of the best that the mortgage industry has to offer,” said MPA editor Ryan Smith. “This list is a who’s who of the industry’s power players and innovators.”

Advice on Lending to Adult Children

Advice on Lending to Adult Children

By Lisa Prevost, OCT 9, 2015

NEW YORK TIMES — Parents often come to the rescue when their adult children need help putting together enough cash for a down payment. Whether they offer financial assistance as a gift or with the expectation of repayment, parents acting from the heart might want to consider a more businesslike approach...

LendingTree Announces Top Ten Customer-Rated Lenders for Q2 2014

LendingTree Announces Top Ten Customer-Rated Lenders for Q2 2014

September 17, 2014 6:13 PM

YAHOO FINANCE — CHARLOTTE, N.C., Sept. 17, 2014 /PRNewswire/ -- LendingTree, the nation's leading online loan marketplace, today announced the top ten customer-rated lenders on its network based on actual customer reviews for the second quarter of 2014. The 'Top Ten' list is based on a weighted average of review rating and volume of customer reviews. Lenders were rated on mortgage rates, fees and closing costs, responsiveness, customer service and overall experience.

LendingTree Announces Top Ten Customer-Rated Lenders for Q1 2014

April 28, 2014 1:11 PM

YAHOO FINANCE — CHARLOTTE, N.C., April 28, 2014 /PRNewswire/ -- LendingTree, the nation's leading online source for competitive loan offers, today announced the top ten customer-rated lenders on its network based on actual customer reviews for the first quarter of 2014. The 'Top Ten' list is based on a weighted average of review rating and volume of customer reviews. Lenders were rated on mortgage rates, fees and closing costs, responsiveness, customer service and overall experience.

LendingTree Recognizes Excellence in Customer Service among Network Lenders Top Ten Customer-Rated Lenders announced for Q4 2012 and Q1 2013

LendingTree Recognizes Excellence in Customer Service among Network Lenders Top Ten Customer-Rated Lenders announced for Q4 2012 and Q1 2013

FRIDAY, MAY 3, 2013

CHARLOTTE, N.C., May 3, 2013 /PRNewswire/ -- LendingTree, the nation's leading online lending exchange, announced the recipients of its annual Lender Excellence in Customer Service Awards which are presented to lenders on the LendingTree network who consistently demonstrate superior customer service.

Loan Qualifications for Retirees

By Lisa Prevost • Published May 2, 2013

NEW YORK TIMES — Retirees trying to obtain a mortgage may find that a pristine credit history and healthy retirement accounts are not enough. Lenders are also looking for a consistent monthly income in line with their usual debt-to-income standards.

Sanford Evans, 75, ran up against this requirement recently when he applied for a $174,000 loan to finance the purchase of an apartment in the Riverdale section of the Bronx. With brokerage accounts exceeding $1 million, a TransUnion credit score of 822, and the ability to make a 40 percent down payment, Mr. Evans didn’t anticipate any problem with qualifying.

Loans for a Niche Market

By Lisa Prevost • Published March 21, 2013

NEW YORK TIMES — If interest-only loans were issued too freely before the foreclosure crisis, their availability now is restricted to a privileged few.

A staple of the jumbo market, interest-only loans continue to be used by affluent borrowers to help them manage irregular cash flow, reap a tax benefit, or free up cash for investment elsewhere.

LendingTree Recognizes Top Ten Customer-Rated Lenders for Q3 2012

LendingTree Recognizes Top Ten Customer-Rated Lenders for Q3 2012

October 17, 2012

LENDINGTREE.COM — CHARLOTTE, N.C., (Oct. 17, 2012) -- LendingTree, the nation's leading online source for competitive home loan offers, has announced the top ten lenders on its network based on customer reviews for the third quarter of 2012. The lenders were rated on mortgage rates, fees and closing costs, responsiveness and customer service from July 1st through September 30, 2012.

National Mortgage News — 2022 mortgage industry predictions

National Mortgage News — Rethinking lead generation for a post-pandemic world

Bankrate — Refinancing after forbearance? Make sure you know the rules

Money — Home Equity is Soaring— if You're Tempted to Borrow Against Your Home, Read this First

Bankrate — Coronavirus is changing home appraisals — and some borrowers don’t need them at all

MoneyWise — Richard Pisnoy quoted in MoneyWise regarding super-low mortgage rates.

The Mortgage Reports — With no loan limits and easy requirements, VA loans are more popular than ever

MoneyWise — Mortgage Rates Hold On at Lowest January Levels Since 2013

Realtor.com — Can I Refinance While Buying a Second Home? Here are the Mortgage Rules

Newsday — Too many people think it's OK to tap home equity to pay monthly bills

Home Loans Blog — Home Equity Loan Products - HELOCs and HELs

MPA — Silver Fin's Richard Pisnoy selected as one of MPA Magazine's Hot 100

U.S. NEWS — What Airbnb Means for Your Mortgage

MPA — Stacey Elshehaby recognized as an "Elite Woman" in Mortgage

MPA — Andrew Weinberg Chosen for MPA's Top 100

MPA — Richard Pisnoy Chosen for MPA's Hot 100

NY TIMES — Advice on Lending to Adult Children

YAHOO FINANCE — LendingTree Announces Top Ten Customer-Rated Lenders for Q2 2014

YAHOO FINANCE — LendingTree Announces Top Ten Customer-Rated Lenders for Q1 2014

NY TIMES — Loans for a Niche Market

NY TIMES — Loan Qualifications for Retirees

LENDINGTREE — LendingTree Recongnizes Top Ten Customer-Rated Lenders for Q3 2012

NEWS LINKS:

Silver Fin Capital Group LLC

11 Grace Avenue, Suite 408,

Great Neck, NY 11021

NMLS ID: 12147

Call 888-758-7346 or 516-466-2930

Fax: 516-570-3801

Serving Connecticut, Florida, New Jersey, New York & Pennsylvania

State of Connecticut: Department of Banking, Licensed Mortgage Broker Number 17302; State of Florida: Office of Financial Regulation, Mortgage Broker License MBR572; State of New Jersey: Department of Banking & Insurance, Residential Mortgage Broker License 0805907; State of Pennsylvania: Department of Banking & Securities, Licensed Mortgage Broker, License 98635; State of New York: Department of Financial Services, (Institution A006520). New York Mortgage Broker Registration 208842.

Loans are provided by third-party lenders and are subject to credit and lender approval. Mortgage brokers are not empowered to make mortgage loans. We seek out the best loan program for your specific situation from our extensive network of wholesale lenders. Lenders pay our fees. In most cases there is no cost to you for services provided by Silver Fin Capital. Copyright © 2014-2022 Silver Fin Capital. Site design and maintenance by DesignStrategies.com.